What is Overseas Investment?

In general parlance, any Investment made outside India by Person Resident in India is considered as “Overseas Investment”.

Overseas Investment enhance the scale and scope of business operations of Indian entrepreneurs by providing global opportunities for growth. These overseas investments are also important drivers of foreign trade and technology transfer thus boosting domestic employment, investment and growth through such interlinkages.

In order to streamline the process and keeping with the spirit of liberalization, Central Government and Reserve Bank of India has issued New Rules and Regulations in suppression of earlier Notification No. FEMA 120/2004-RB dated July 07, 2004 [Foreign Exchange Management (Transfer or Issue of any Foreign Security) (Amendment) Regulations, 2004] and Notification No. FEMA 7 (R)/2015-RB dated January 21, 2016 [Foreign Exchange Management (Acquisition and Transfer of Immovable Property Outside India) Regulations, 2015. (Collectively referred as OI1.0 or Earlier Notifications for the purpose of this Article)

Guiding Regulations:

| Category | Particulars | Issuer | Notification No and Date |

|---|---|---|---|

| Rules | Foreign Exchange Management (Overseas Investment) Rules, 2022 | Central Government | Notification No. G.S.R. 646(E) dated August 22, 2022 |

| Regulations | Foreign Exchange Management (Overseas Investment) Regulations, 2022 | Reserve Bank of India | Notification No. FEMA 400/2022-RB dated August 22, 2022 |

| Master Directions | Foreign Exchange Management (Overseas Investment) Directions, 2022 | Reserve Bank of India | A.P. (DIR Series) Circular No.12 dated August 22, 2022 |

| Regulations | Liberalised remittance Scheme | Reserve Bank of India | FED Master Direction No. 7/2015-16. updated as on August 23,2022 |

| Master Direction | Master Direction – Reporting under Foreign Exchange Management Act, 1999 | Reserve Bank of India | Reserve Bank of India Updated as on August 22,2022 |

Overseas Investment 2.0 has brought significant changes with respect to earlier notifications in place. It also brought more clarity with respect to some of the aspects. Some of the significant changes are mentioned below,

- more clarity on Round Tripping issues/Investment in IFSCA by Person Resident In India

- enhanced clarity with respect to various definitions;

- introduction of the concept of “strategic sector”;

- dispensing with the requirement of approval for:

- deferred payment of consideration;

- investment/disinvestment by persons resident in India under investigation by any investigative agency/regulatory body;

- issuance of corporate guarantees to or on behalf of second or subsequent level step down subsidiary (SDS);

- write-off on account of disinvestment;

- introduction of “Late Submission Fee (LSF)” for reporting delays

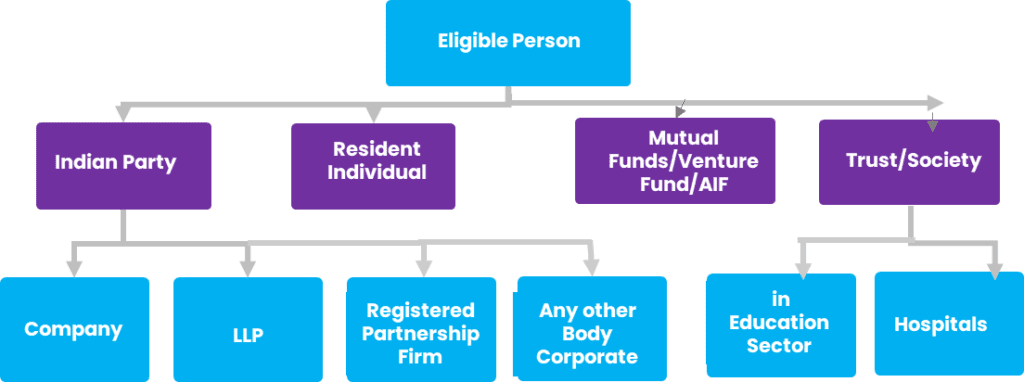

As per RBI Guidelines, Following are the eligible persons to make an Overseas Investment

Each one of the above category can invest in Overseas with certain limit and conditions depending on the type of instrument, they would like to invest.

As per RBI Guidelines, Overseas Investment (“OI”) not only include investment in shares/ securities but it also include Foreign Commitment made through guarantees, Loan etc.

Following are the different kinds of Overseas Investments,

A. Overseas Direct Investment (“ODI”)

Overseas Direct Investment is the term used for Strategic Investment. Following are investments that are considered as ODI and should be routed through ODI route.

1.Acquisition of Unlisted Entity Equity capital,

2.Subscription as a part of Memorandum of Association

3.Investment in 10% or more of the paid-up equity capital of a listed foreign entity

4.Investment with control where investment is less than 10% of the paid-up equity capital of a listed foreign entity

B. Overseas Portfolio Investment (“OPI”)

Overseas Portfolio Investment is the term used for other than Strategic Investment. It refers to any investment other than ODI, but excluding the following,

1.any unlisted debt instruments; or

2.any security which is issued by a person resident in India who is not in an IFSC; or

3.any derivatives unless otherwise permitted by Reserve Bank; or

4.any commodities including Bullion Depository Receipts (BDRs).

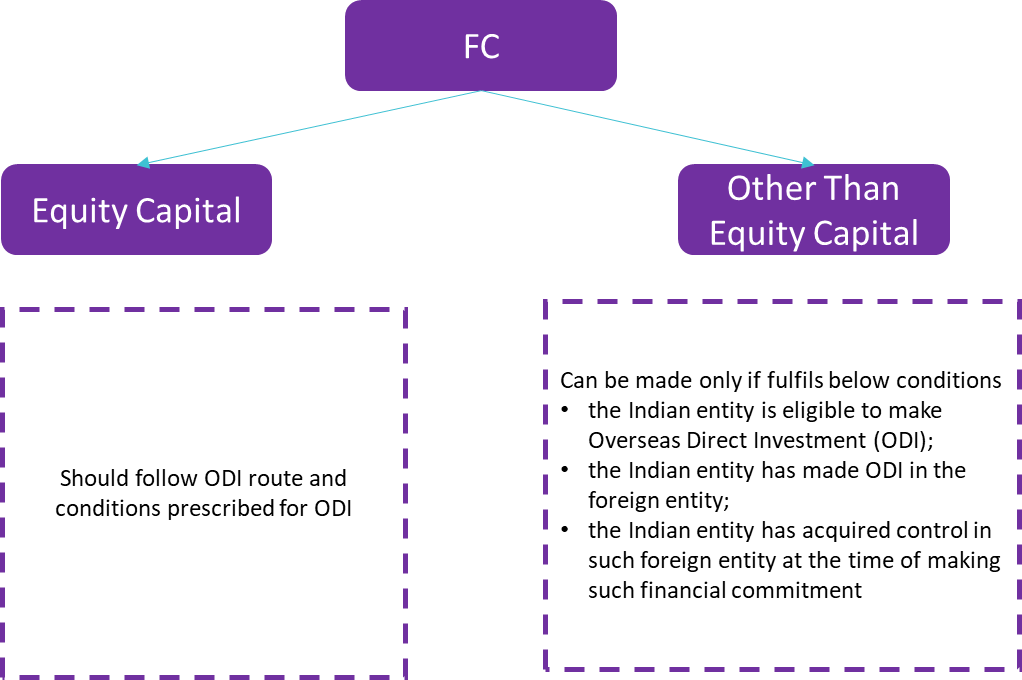

C. Financial Commitment (“FC”)

Financial Commitment is a broader aspect than ODI and cover following

- Investment by way of ODI as mentioned above,

- debt other than Overseas Portfolio Investment (OPI) and

- non-fund based facility or facilities extended by it to all foreign entities

FC= ODI +Debt excluding OPI +Non Fund based facility

OI = FC +OPI

Indian Entity can give Financial Commitment up to 400% of its Net worth as per last Audited Balance sheet.

Limit prescribed is over all limit for all Financial Commitments made in all Foreign entities taken together at the time of undertaking such commitment

A. Debt

Debt can be given only if Indian entity already have capital and control in the Foreign Entity,

- loans are duly backed by a loan agreement

- the rate of interest shall be charged on an arm’s length basis

B. Guarantee

Following guarantees can be given to Foreign Entity or its step down subsidiary, only if Indian entity already have capital and control in the foreign Entity,

- corporate or performance guarantee by such Indian entity;

- corporate or performance guarantee by a group company of such Indian entity in India, being a holding company (which holds at least 51 per cent. stake in the Indian entity) or a subsidiary company (in which the Indian entity holds at least 51 per cent. stake) or a promoter group company, which is a body corporate;

- personal guarantee by the resident individual promoter of such an Indian entity;

- bank guarantee, which is backed by a counter-guarantee or collateral by the Indian entity or its group company as above, and issued, by a bank in India

In case of Guarantee by a resident individual promoter, the same shall be counted towards the financial commitment limit of the Indian entity

In case of performance guarantee, 50 %. of the amount of guarantee shall be reckoned towards the financial commitment limit

Pledge/Charge by Indian Entity in which it has made ODI

| Security by Indian Entity | In whose Favour | Facility availed | Amount reckoned as FC |

|---|---|---|---|

| Pledge the equity capital of the foreign entity /its SDS outside India | AD bank or a public financial institution in India or an overseas lender | Fund/non-fund based facilities for Indian entity. | NIL |

| Fund/non-fund based facilities for any foreign entity/its SDSs outside India. | The value of the pledge or the amount of the facility, whichever is less. | ||

| debenture trustee registered with SEBI in India | Fund based facilities for Indian entity. | NIL | |

| Create charge on its assets (other than A above) in India [including the assets of its group company or associate company, promoter and / or director]. | AD bank or a public financial institution in India or an overseas lender | Fund/non-fund based facility for any foreign entity/its SDS outside India | The value of charge or the amount of the facility, whichever is less |

| debenture trustee registered with SEBI in India | fund/non-fund based facilities for Indian entity. | NIL | |

| Create charge on the assets outside India of the foreign entity/ its SDS outside India. | AD bank or a public financial institution in India or an overseas lender | Fund/non-fund based facility for any foreign entity/its SDS outside India | The value of the charge or the amount of the facility, whichever is less. |

| Fund/non-fund based facility for Indian Entity | Nil | ||

| debenture trustee registered with SEBI in India | Fund based facilities for Indian entity. | Nil |