As per OI 2.0 Regulations, Resident Individual is allowed to invest in ODI or OPI as per manner prescribed. All such Overseas Investments are subject to overall limit prescribed under Liberalized Remittance Scheme (“LRS”) of the Reserve Bank, which is currently USD 2,50,000 per financial year.

LRS Scheme is available only for Resident Individuals including minors. LRS scheme allows to invest in below permissible transactions up to USD 2,50,000 per financial year.

Permissible Transactions under LRS are as follows,

1.opening of foreign currency account abroad with a bank;

2.acquisition of immovable property abroad

3.Overseas Direct Investment (Read Part 1 of 3 – Overseas Investment to understand the terms in detail)

4.Overseas Portfolio Investment (Read Part 1 of 3 – Overseas Investment to understand the terms in detail)

5.extending loans including loans in Indian Rupees to Non-resident Indians (NRIs) who are relatives as defined in Companies Act, 2013

clubbing is not permitted by other family members for capital account transactions such as opening a bank account/investment , if they are not the co-owners/co-partners of the overseas bank account/ investment

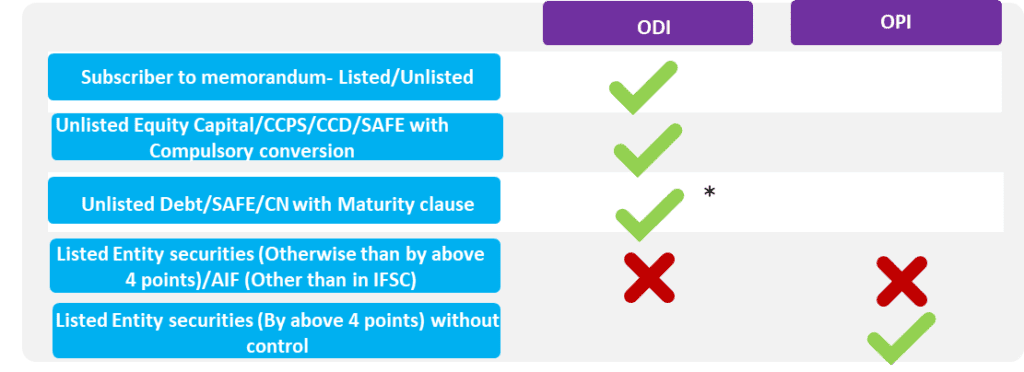

Following table summarizes investment by Resident Individual within overall LRS Limit

| Category | Type of Instruments | % of Holding less than 10% (Without Control) | % of Holding less than 10% (With Control) | % of Holding more than 10% |

|---|---|---|---|---|

| Unlisted Entities | Equity | Qualifies as ODI | Qualifies as ODI | Qualifies as ODI |

| Compulsorily Convertible Instruments (CCPS)/CCD | Qualifies as ODI | Qualifies as ODI | Qualifies as ODI | |

| Perpetual Capital (Capital Contribution) | Qualifies as ODI | Qualifies as ODI | Qualifies as ODI | |

| SAFE Note without Maturity Clause | Qualifies as ODI | Qualifies as ODI | Qualifies as ODI | |

| SAFE Note without Maturity Clause/CN without mandatorily conversion clause/ Debt Securities | Qualifies as FC, RI need to fulfil conditions prescribed for FC including already have Equity capital/ control conditions etc | Qualifies as FC, RI need to fulfil conditions prescribed for FC including already have Equity capital/ control conditions etc | Qualifies as FC, RI need to fulfil conditions prescribed for FC including already have Equity capital/ control conditions etc | |

| Listed Entities | Listed Equity Capital – Subscriber to Memorandum | Qualifies as ODI | Qualifies as ODI | Qualifies as ODI |

| Listed Equity Capital – Investor | Qualifies as OPI | Qualifies as ODI | Qualifies as ODI | |

| Unlisted Debt Instruments | Qualifies as ODI | Qualifies as ODI | Qualifies as ODI | |

| AIF | Units of AIF | Qualifies as OPI | Qualifies as OPI | Qualifies as OPI |

| Units of AIF in IFSC | Qualifies as OPI | Qualifies as OPI | Qualifies as OPI |

* This will qualify as FC, can be done only if the Indian entity is eligible to make Overseas Direct Investment (ODI); (ii) the Indian entity has made ODI in the foreign entity; (iii) the Indian entity has acquired control in such foreign entity at the time of making such financial commitment.

If investment qualifies as ODI, then it should be properly routed through ODI route which requires form FC Submission to AD bank and regular reporting requirements, Whereas if investments qualifies as OPI, Reporting requirements are very minimal.

Swap of securities:

For Resident Individuals and Indian Entity, In case of Swap of of securities both the legs of transaction shall comply with FEMA provisions, as applicable

However in case of resident individuals, where swap of securities results in acquisition of any equity capital which is not in conformity with the OI Rules/Regulations, e.g., ODI in foreign entity engaged in financial services activity, foreign entity having a subsidiary/SDS, etc., such equity capital must be disinvested within a period of six months from the date of such acquisition.

Employee Stock Ownership Plan or Employee Benefits Scheme:

OI 2.0 regulations allows Resident Individuals to hold/acquire shares or interest under Employee Stock Ownership Plan or Employee Benefits Scheme.

Generally, resident individuals are not allowed to invest in Financial services Entity. However, such restrictions is not applicable if it is acquired through ESOP plan/benefit scheme.

Therefore, whether or not such foreign entity is engaged in financial services activity or has subsidiary or step down subsidiary where the resident individual has control, resident Individual to acquires shares or interest under Employee Stock Ownership Plan or Employee Benefits Scheme.

Such acquisition of the shares/interest in an overseas entity under the scheme offered either directly by the issuing entity or indirectly through a Special Purpose Vehicle (SPV) /SDS.

Where the investment qualifies as OPI, the necessary reporting in Form OPI shall be done by the employer concerned in accordance with regulation 10(3) of OI Regulations. Where such investment qualifies as ODI, the resident individual concerned shall report the transaction in Form FC

Though there is no limit on the amount of remittance made towards acquisition of shares/interest under ESOP/Employee Benefits Scheme or acquisition of sweat equity shares, such remittances shall be reckoned towards the LRS limit of the person concerned

GIFT:

For Resident Individual, Gift is allowed as per below table

| Donor | Foreign Securities | Other Than Foreign Securities | Remarks |

|---|---|---|---|

| Person resident in India | Allowed | Not Allowed | Person resident in India has to be relative as per Companies Act, 2013 Such Foreign Securities can be of Financial/Non financial Sector It can also be of Foreign entity in which resident Individual has control |

| Person resident Outside India | Allowed | Not Allowed | It has to comply with Foreign Contribution (Regulation) Act, 2010 |

Inheritance:

For Resident Individual, Inheritance is allowed as per below table

| Donor | Foreign Securities | Other Than Foreign Securities | Remarks |

|---|---|---|---|

| Person resident in India | Allowed | Not Allowed | In case, Securities acquired through inheritance from Person Resident in India should have acquired through FEMA provision |

| Person resident Outside India | Allowed | Not Allowed | NA |

Acquisition of foreign securities by way of inheritance or gift in accordance with above shall not be reckoned towards the LRS limit and hence, shall not require reporting under LRS

Following table summarizes Reporting requirements at each stage

| Route | Time | Scenario | Forms | Time Limit |

|---|---|---|---|---|

| ODI | One Time | At the time of making Investment | Form FC | at the time of undertaking outward remittance or financial commitment, whichever is earlier |

| Making Financial Commitment | ||||

| Undertaking restructuring | Within 30 days from the date of such restructuring. | |||

| Disinvestment | within 30 days from the date of receipt of disinvestment proceeds | |||

| ODI Post Investment | Submission of Share certificates or other relevant documents | Within 6 months from date of effecting remittance | ||

| Yearly | Reporting on Foreign Assets/Liabilities | Annual Return on Foreign Liabilities and Assets (FLA) | On or Before July 15th | |

| Reporting on Annual performance on Investments Made | Annual Performance Report (APR) | On or Before 31st Dec |

Delay in Reporting post OI 2.0:

In case of any delay in reporting in any of the above filing, then person may make such submission or filing along with Late Submission Fee (LSF) within such period as may be advised. However, such facility can be availed within a maximum period of 3 years from the due date of such submission or filing.

Delay in Reporting pre OI 2.0:

In case of any delay in reporting pre OI2.0 (or in other words OI 1.0), , then person may make such submission or filing along with Late Submission Fee (LSF) within such period as may be advised. However, such facility can be availed within a maximum period of 3 years from the date of publication of OI Regulations in the Official Gazette

| Types of delay | LSF Amount |

| Form ODI Part-II/ APR, FLA Returns, Form OPI, evidence of investment or any other return which does not capture flows or any other periodical Reporting | INR 7,500 |

| Form ODI-Part I, Form ODI-Part III, Form FC, or any other return which captures flows or returns which capture reporting of non-fund based transactions or any other transactional reporting | 7500 +(0.025%*amount involved in delay reporting*n) |