Startup generally needs to have a overseas arms for any of the following reasons,

- Investor stipulated conditions to have overseas Holding Company

- Better business opportunities

- Better Investor attraction

However, in OI 1.0, Startup were facing few issues which are outlined below,

Issues 1- Round Tripping:

Round Tripping is a colloquial term referring to a situation where:

(a) an Indian Resident invests in an Overseas Entity, which subsequently sets up a Subsidiary in India or

(b) where investments are made in an Overseas Entity, and such investments are invested back into the Indian entity

Round Tripping is a common model in cases of Externalization. It is interesting to note that the word round tripping has not been defined in FEMA Regulations. However, RBI has indirectly placed restrictions on such transactions vide. FAQ on ODI No 64.

Extracts of the FAQ as follows:

RBI FAQ No 64 : Can an Indian Party (IP) set up a step-down subsidiary/joint venture in India through its foreign entity (Wholly Owner Subsidiary “WOS”/ Joint Venture “JV”), directly or indirectly through step-down subsidiary of the foreign entity?

No, the provisions of Notification No. FEMA 120/RB-2004 dated July 7, 2004, as amended from time to time, dealing with transfer and issue of any foreign security to Residents do not permit an IP to set up Indian subsidiary(ies) through its foreign WOS or JV nor do the provisions permit an IP to acquire a WOS or invest in JV that already has direct/indirect investment in India under the automatic route. However, in such cases, IPs can approach the Reserve Bank for prior approval through their Authorized Dealer Banks (“AD Banks”) which will be considered on a case to case basis, depending on the merits of the case

Therefore any founder which intends to setup overseas Holding Company which subsequently set up Indian Subsidiary cannot be done without prior RBI approval, because of restriction placed in FAQ 64.

Solutions in OI 2.0

In order to promote Externalization/Flip Structure for Start-ups, Government of India and RBI has brought certain clarity through change in restrictions already placed.

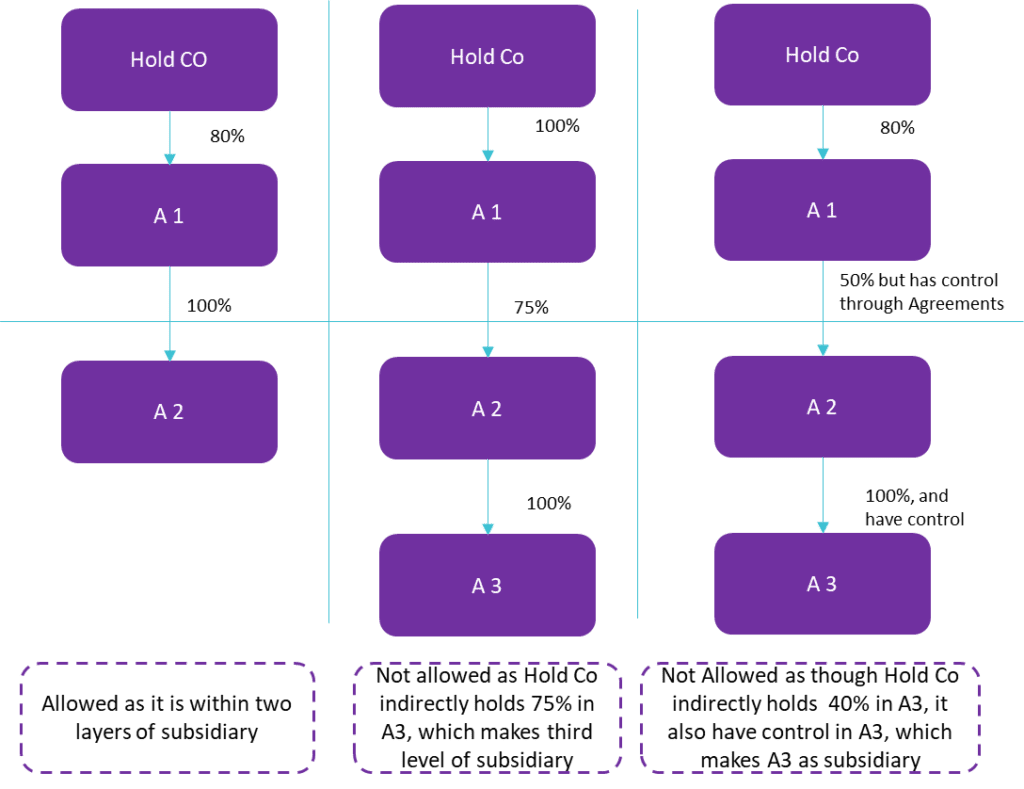

In OI 2.0, Restrictions has been placed only if anyone invests in Foreign entity as Foreign Commitment, which has either invested or invests to India either directly or indirectly, resulting in a structure with more than two layers of subsidiaries.

Therefore, no Round Tripping issues if the foreign Entity has less than 2 layers of subsidiaries. This is a welcome move to promote and encourage the Start-up which needs to have overseas Subsidiary. Subsidiary is defined to include any entity in which Foreign Entity has control. Few illustrations to explain above scenario

Issues 2- Net worth Criteria:

OI regulations allows person resident in India to make Financial Commitment to the extent of 400% of its Net worth as per last Audited Balance Sheet. The limit is same as per earlier and current regulations.

In earlier regulations Net worth is defined to include Paid up capital and Free Reserves. However, Free Reserves is not defined. This had led to ambiguity whether Free reserves includes Share Premium or not.

As per Companies Act, 2013 Free Reserves does not include Share Premium. However, the definition of Net worth in Companies Act, 2013 includes share premium.

Therefore, Authorised Dealers were taking a view that free reserves does not including share premium relying on Companies Act, 2013 definition.

This has placed restriction on the early stage companies to invest in overseas, whose Net worth is negative excluding share premium.

Solutions in OI 2.0

OI 2.0 removes all ambiguity related to Net worth and brough more clarity in definition of Net worth. Net worth is defined to mean Net worth as per companies Act, 2013, which includes share premium. Extracts of 2(57) of Companies Act, 2013 is as follows:

“net worth” means the aggregate value of the paid-up share capital and all reserves created out of the profits ,securities premium account and debit or credit balance of profit and loss account], after deducting the aggregate value of the accumulated losses, deferred expenditure and miscellaneous expenditure not written off, as per the audited balance sheet, but does not include reserves created out of revaluation of assets, write-back of depreciation and amalgamation

Investment in international Financial Services Centre (IFSC) is gaining importance in récent days. Government of India operationalized International Financial Services Centre (IFSC) at GIFT Multi Services SEZ in April 2015. The Union Budget 2016 provided competitive tax regime for the IFSC at GIFT SEZ

OI 2.0 removes all ambiguity related to investment in IFSC. Some of the important clarity is as follows,

- As per Schedule V of Foreign Exchange Management (Overseas Investment) Rules, 2022 , an person resident in India may make contribution to an investment fund or vehicle set up in an IFSC and same will be considered as OPI. Therefore, act specifically allows any resident to invest in investment Vehicle set up in IFSC.

- If a resident wants to set up entity in IFSC, same will be considered as ODI and all ODI limits specified in OI 2.0 will be applicable.

- an Indian entity not engaged in financial services activity in India, making ODI in a foreign entity, which is directly or indirectly engaged in financial services activity, except banking or insurance, need not meet the net profit condition, which was otherwise required.

- In the case of an ODI Financial services sectors, generally approval from concerned Regulator will be required . However, if such ODI is made in IFSC, approval by the financial services regulator concerned, wherever applicable, shall be decided within forty-five days from the date of application failing which it shall be deemed to be approved

| Investor | Investee Entity | Conditions to be fulfilled | Remarks |

|---|---|---|---|

| Resident individual | Investment Vehicle | Within LRS Limit | Considered as OPI |

| LLP/Company for any other reasons other than above (“Non Financial Entity) | Within LRS Limit | Considered as ODI | |

| Non Financial Entity | Investment Vehicle | Within OPI limit | Considered as OPI |

| Investment Vehicle as Sponsor | Within ODI limit | Considered as ODI | |

| Other Financial Entity | Within ODI/OPI limit | Considered as ODI/OPI depending on unlisted/listed and having control or not | |

| Other Non Financial entity | •Within ODI limit | Considered as ODI/OPI depending on unlisted/listed and having control or not | |

| Financial Entity) | Investment Vehicle | Within OPI limit | Considered as OPI |

| Investment Vehicle as Sponsor | •Within ODI limit •Financial Regulator approval is required. If no approval is given within 45 days, it is deemed approved. •Track record of net profit for the period of three years | Considered as ODI | |

| Other Financial Entity | •Within ODI limit •Financial Regulator approval is required. If no approval is given within 45 days, it is deemed approved. •Track record of net profit for the period of three years | Considered as ODI | |

| Other Non Financial entity | •Within ODI limit | Considered as ODI/OPI depending on unlisted/listed and having control or not |

OI 2.0 has brought few changes to entity engaging in Financial services sectors.

Clarity in Financial Services Entity:

It has brought clarity in Financial Services Activity. Earlier Notification did not define what constitute Financials Services Activity. This has led to many interpretations and confusions.

OI 2.0 has removed this ambiguity by bringing in more clarity of Financial services Activity.

As per OI 2.0, an Entity will be considered as operating In Financial services Activity in Host Country, if it undertakes an activity, which if carried out by an entity in India, requires registration with or is regulated by a financial sector regulator in India

By above definition, an overseas entity need not be mandatorily registered/regulated to fall under Financial services activity. If it carries any activity, which requires to be registered or regulated as per Indian Law, then such entity even though not registered/regulated in overseas entity will be still considered as Financial Services Activity.

Unregulated Entity:

In earlier Notifications OI 1.0, Unregulated entity cannot invest in overseas entity engaging in Financials services sector. Only Indian Entity engaging in Financial services sector allowed to invest in Overseas Financial Services Sector.

OI 2.0 has been modified to allow even unregulated Indian entity to invest in Overseas Financial services sector within certain conditions to be fulfilled.

Entity in Financial Services sector investing in Financial Services sector

| Investor | Criteria | OI 1.0 | OI 2.0 |

|---|---|---|---|

| ODI in Financial Service Activity | Net Profit Criteria | •Entity should have a track record three years net profits preceding three financial years | No change in Net profit criteria. Entity should have three net profit preceding three years. However, relaxation in Net profit criteria has been brought in due to Covid Impact. If the Indian Entity does not have Net profit due to Covid for FY 2020-2021 to 2021-2022, ODI in IFSC Financial Services Activity: Same as above |

| Registration Criteria | Entity has to be “Registered” with regulatory authority in India for conducting the financial sector activities | Entity has to be “registered with or regulated” by a financial services regulator in India ODI in IFSC Financial Services Activity: Same as above | |

| Approval from Regulatory Authority | Mandatory approval from Regulatory Authority is required | the Indian entity has obtained approval as may be required from the regulators of such financial services activity, both in India and the host country or host jurisdiction, as the case may be, for engaging in such financial services Further, in case of ODI by Banking and Non Banking Financial Sector regulated by the Reserve Bank Of India, it should fulfill conditions stipulated by RBI. ODI in IFSC Financial Services Activity: If approval is not received within 45 days, it will be deemed approval from Regulatory |

Entity in Financial Services sector investing in Non Financial Services sector

| Investor | Criteria | OI 1.0 | OI 2.0 |

|---|---|---|---|

| ODI in Non Financial Service Activity | Net Profit Criteria | •Entity should have a track record three years net profits preceding three financial years | It is ssubject to the guidelines issued by the respective regulator. No other specific conditions are applicable |

| Approval from Regulatory Authority | Mandatory approval from Regulatory Authority is required |

Entity in Non Financial Services sector investing in Financial Services sector

| Investor | Criteria | OI 1.0 | OI 2.0 |

|---|---|---|---|

| ODI in Financial Service Activity (Other than Banking and Insurance) | Net Profit Criteria | •OI 1.0 did not allow unregulated Financial services Activity to invest in Financial services Activity overseas | Entity should have three net profit preceding three years. However, relaxation in Net profit criteria has been brought in due to Covid Impact. If the Indian Entity does not have Net profit due to Covid for FY 2020-2021 to 2021-2022, ODI in IFSC Financial Services Activity Other than Banking and Insurance: Entity need not to have net profit for preceding three years |

Entity in Non Financial Services sector investing in Non Financial Services sector

| Investor | Criteria | OI 1.0 | OI 2.0 |

|---|---|---|---|

| ODI in Non Financial Service Activity | No Specific criteria | •General guidelines applicable for making any overseas investments I | General guidelines applicable for making any overseas investments |

Read out more on Overview – Overseas Investment Part 1 of 3